The Better Letter: Trading Stories

Bold stories, told and sold

The story may be apocryphal, but Maria Konnikova describes the French poet Jacques Prévert improving a blind beggar’s signage and fortunes. In place of “Blind man without a pension,” Prévert flipped the sign over and wrote, “Spring is coming, but I won’t see it.” For all of us, all too much of the time, as Ursula K. Le Guin outlined, “Truth is a matter of the imagination.”

We love stories, true or not, from cradle to grave. We all trade them and try to control our narratives. Stories are crucial to how we make sense of reality. They help us to explain, understand, and interpret the world around us. Stories take us to a land of make-believe, both figuratively and literally. I have a few for you this week.

If you like The Better Letter, please subscribe and share it using the buttons below.

Thanks for stopping by.

Long-Term Losses

I had never before heard the trading floor go silent.

In 1998, the Merrill Lynch fixed income trading floor was a gigantic room with a 30-foot ceiling, comprising most of the seventh floor of the North Tower of the World Financial Center in lower Manhattan. On a normal day, it was teeming with noise and activity. Every work station had multiple phones, multiple computers, and multiple Bloomberg terminal screens.

When markets were moving, it was raucous with noisy trading activity. When markets weren’t moving, it was just raucous, with balls and insults thrown about with equal abandon.

By 1998, I no longer worked on the trading floor or at world headquarters, but I still worked for Mother Merrill. I was back in New York and on the trading floor that day by pure happenstance. The cavernous room contained hundreds of people, ginormous egos, and thousands of machines. Billions of dollars changed hands there every day. Any trade under $5 million was an odd-lot.

Before that September day, the quietest I had ever heard the trading floor was a Friday afternoon when a trader and a salesman, among whom there was always tension anyway (I was on the sales side*, but the traders had a point – they had P&L, we essentially only had P), argued about whether the salesman cared about his (perfect) hair too much. A stack of hundreds totaling $10,000 was slapped down to make the case that the salesman wouldn’t shave his head because he loved his hair too much. The woman at the work station next to mine whispered that she would shave every hair on her body for $10,000. The head was not shaved. We watched the confrontation, transfixed.

The not normal day I’m talking about was quieter still.

The only sound that morning was the whirring of fax machines spitting out page after page of bid lists containing securities Long-Term Capital Management needed to sell in the firm’s capitulation to the markets and to the inevitability of its demise. We all observed in stunned silence, watching the pages cascade into waiting trays around the floor, recognizing that the market liquidity LTCM had assumed was a chimera. The firm was toast.

LTCM was an early hedge fund, populated by the self-proclaimed smartest guys in the room and, to be fair, a few who had well established their intellects by, among other things, winning Nobel Prizes, teaching at Harvard or Stanford, or being vice-chair of the Fed.

The firm was founded by John Meriwether, a legendary trader who had left Salomon Brothers in a scandal over bid-rigging in U.S. Treasury auctions of two-year notes. I don’t know, but my guess is his biggest disgrace over the scandal related to his getting caught.

Because Merrill was involved in marketing LTCM – we were supposed to convince our institutional accounts to give LTCM money – I was in an early pitch meeting. It was very straightforward. There was no deck. There were jokes and back-slapping. Basically, Meriwether stood up and told those assembled that he would make them a boat-load of money. But he didn’t say “boat.” And there was an adjective in front of it that began with “f” and ended with “in’.”

At LTCM, it all worked right up until it didn’t. Returns at the firm level had exceeded 40 percent per annum. But a quick and unhedged market turn (the Russian bond market collapsed in August of 1998) coupled with enormous leverage spelled death for the firm.

LTCM killed it for four years and then got killed.

As Victor Fleischer famously put it, “hedge funds are a compensation scheme masquerading as an asset class.” The initial hedge fund pitches (as with LTCM) generally focused on outsized returns that promised more than enough juice to justify the exorbitant fees – the infamous “two and twenty.”

Performance, most spectacularly at LTCM, but not just there, didn’t end up living up to the hype. Over the past ten years, hedge fund returns have been crushed by stocks and roughly equaled by bonds.

When analyzed on an asset-weighted basis, hedge fund returns are even worse. As Simon Lack documented in his book, The Hedge Fund Mirage, if all the money that has ever been invested in hedge funds had been invested in U.S. Treasury bills instead, the overall results would have been twice as good.

There are a few great hedge funds, but none of them is taking money from the likes of you or me.

Since marketing hedge funds on outsized performance failed, the focus of the sales pitch shifted to non-correlation, risk control, and outperformance in difficult markets. The shills began to say that the lousy performance numbers hedge funds put up aren’t the numbers that matter.

The full body of available evidence compellingly shows that hedge funds haven’t lived up to the more nuanced hype either. Hedge fund promise far outpaces performance – by any measure. There is no evidence that hedge funds outperform in volatile or down markets. “Despite promises of better and less correlated returns, hedge funds failed to deliver significant benefits to any of the pension funds we reviewed,” one prominent study found. “Our analysis suggests that hedge funds as an investment product fall short on both of their major selling points: outsized returns that offset the exorbitant fees and uncorrelated returns that smooth out market volatility and offer investors protection during economic downturns.”

Hedge fund performance may be dreadful, but investment in them does serve one clear purpose. Meir Statman provided this added explanation: “Investments are like jobs, and their benefits extend beyond money. Investments express parts of our identity, whether that of a trader, a gold accumulator, or a fan of hedge funds.” He then explained that people frequently invest in hedge funds for the same reason they buy a Rolex – they are expressions of status available only to the wealthy. This status is fundamental to hedge fund allure despite poor performance, and hedge fund marketing takes full advantage.

In other words, hedge fund investing is a terrible idea if your goal is investment-related. But if you want to appear rich and don’t mind losing money to do it, hedge funds might be just the ticket.

_______________

* I had basically the same job that Michael Lewis held at Salomon Brothers and described in his terrific first book, Liar’s Poker.

Trust the Process

Teachers are frustrated about teaching online during these days of required sheltering in place. Student engagement is far from what it needs to be and teachers are struggling to hold their students accountable, especially when parents aren’t willing or able to help. It’s also not the sort of teaching they signed up for and love.

Dedicated parents are struggling, too.

Math anxiety is common, among students and parents.

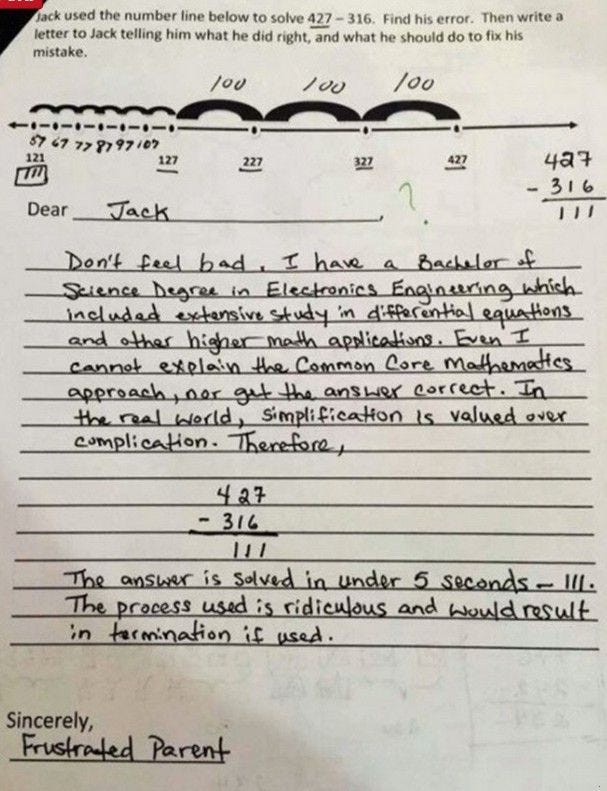

The current crisis has also exacerbated problems that already existed, such as parental resistance to “Common Core” math (see below for a representative illustration).

Areas of constant discord are Common Core’s process-driven resistance to the use of shortcuts (like cross-multiplication of fractions, for example), the memorization of facts before understanding is demonstrated, and its insistence upon students showing their work (see below).

While Common Core principles have all too frequently been implemented poorly, these principles make sense and are well-grounded. And, obviously, mathematical acuity and understanding are in short supply…

…even at The New York Times.

Students of behavioral economics are well acquainted with “the bat and ball problem.”

A bat and ball cost $1.10.

The bat costs one dollar more than the ball.

How much does the ball cost?

The correct answer is $.05. As Daniel Kahneman and Shane Frederick observed, the intuitive conclusion most jump to is $.10. In Thinking, Fast and Slow (it’s fascinating how often the book title is written without the comma), Kahneman used the bat and ball problem to introduce the book’s major theme: the distinction between fluent, spontaneous, fast “System 1” thinking, and effortful, reflective, slow “System 2” thinking. In general, we are too willing to lean on System 1, which gets us into trouble.

A key element of “Common Core” thinking is to require that students slow down and get “System 2” engaged. Like good investment theory and Sam Hinkie, it emphasizes process over outcome. Common Core doesn’t eliminate short-cuts or minimize getting the right answers, it merely emphasizes the importance of understanding why the answer is right so students can build on that knowledge as they study more advanced math.

In other words, trust the process.

Too Long-Term

I heard a pitch this week that suggested various managers and firms are making “100-year plans.” I’m a big believer in investing for the long-term and a big believer in long-range planning. But care and common sense are required.

In the summer of 1993, I was part of the second 100-year bond issuance ever. The issuer was Disney. The 30-year U.S. Treasury bond, the benchmark for other long-term securities, had recently set a then-record low in yield of 6.52 percent. The new issuance paid a coupon of 7.55 percent and priced at a slight discount for a yield that was 95 basis points more than that of the 30T.

Fixed income portfolios were desperate for convexity at that time as falling rates and the mortgage prepayments they precipitated were causing mortgage bonds to be paid off sooner than desired. Corporate bond issuers, guessing they might never see interest rates that low again, wanted to lock up cheap financing for as long as they could.

In those days, my first call each morning was to a market veteran pension manager, nearing retirement, who had become my mentor. I always learned from Ray and used his morning insights to build my own points of view. He taught me to read the tabloids to make sure I understood what Americans not keyed into Wall Street were thinking. He explained how he had counted and kept a record of delivery trucks entering the city on his morning commute for years, as a way to check government productivity statistics.

He taught me to test everything and to be skeptical of everyone because everybody talks their book.

As I talked with Ray about the Disney offering, I emphasized portfolio construction, analytics, and the power of convexity. He heard me out and then put me in my place.

“If, 100 years ago, I had purchased a 100-year bond issued by the world’s leading entertainment company,” he said, “today I’d be looking to have my principal repaid by the world’s leading player-piano manufacturer.”

So much for “100-year plans.”

Totally Worth It

Cross-border geriatric love despite social distancing. An Ohio teen got a multi-million-dollar stimulus check. If you don’t have enough to be afraid of. Barstool Sports founder Dave Portnoy lost a boat-load of money trading stocks, because of course he did.

Curt Smith of Tears for Fears performs “Mad World” with his talented daughter.

Sheltering in place isn’t always going well.

The best photos of the decade. Museums share photos of their creepiest items.

The apocalypse is nigh.

Benediction

Nashville studio musicians are legendary, for good reason. A group of 30 Nashville studio singers got together and recorded an acapella, cellphone choir version of the hymn, It Is Well With My Soul (h/t David French). Horatio Spafford wrote it in 1873 after learning that his children had been lost at sea. It’s quite a story. The song makes a glorious benediction.

Contact me via rpseawright [at] gmail [dot] com or on Twitter (@rpseawright). Don’t forget to subscribe and share.

Issue 10 (April 24, 2020)