Fear Not

Trading on fear.

I was recently asked about Harry Dent and his apocalyptic forecast for the market. I replied, “Which one?”

Dent called for “the collapse of our lifetime” – an 86 percent loss for the S&P 500; 86 percent on the Russell 2000; 92 percent on the Nasdaq – by June 2023. That didn’t happen, obviously, so now he says it’s coming in 2024.

He's a compelling speaker who exudes impressive confidence, especially considering his history.

In 1999, just before the Great Financial Crisis and a huge market drop, he wrote The Roaring 2000s: Building the Wealth and Lifestyle You Desire in the Greatest Boom in History. Dent predicted that the stock market would experience a huge boom during the first decade of the new century, reaching 35,000 on the Dow. The DJIA closed 1999 at 11,497 and 2009 at 10,428. So, he missed it by a mile. The DJIA did reach 35,000 in June 2021, but Dent had long been a permabear by then.

In The Next Great Bubble Boom: How to Profit from the Greatest Boom in History: 2006-2010, published in January 2006, Dent doubled down on his earlier predictions for the 2000s and called for big gains through the rest of the decade. He missed this one, too.

In late 2008, Dent published another book, The Great Depression Ahead: How to Prosper in the Crash Following the Greatest Boom in History, moving into the “doom and gloom” business. Bad move. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. It closed today (1.25.24) at 38,049.

In December of 2016, Dent went on CNBC to insist the Dow would “end up between 3,000 and 5,000 a couple years from now.” The Dow closed at 23,327 a couple of years later – the end of 2018 – and has not dropped below 19,000 since the prediction.

In June 2017, Dent predicted a “once in a lifetime” crash in the stock market, the economy, and in real estate over the following three years. Dent got a big market decline in 2020, but because of Covid, not for any of the reasons he cited. Moreover, by the end of that year, the decline (and more) had been recovered.

In March 2021, Dent called for a nearly 50 percent drop in the S&P 500 by June. Didn’t happen. In July 2021, he followed up with a prediction that equities would drop by 80 percent in the fall, which didn’t happen, either.

In late August 2022, he claimed that “[t]he biggest crash of our lifetime is in progress,” but it wasn’t. In November, he pushed it back to early 2022. Also, wrong. Which returns us to his more recent apocalyptic visions.

This sort of nonsense is the subject of this week’s TBL.

If you like The Better Letter, please subscribe, share it, and forward it widely.

NOTE: Some email services may truncate TBL. If so, or if you’d prefer, you can read it all here. If it is clipped, you can also click on “View entire message” and you’ll be able to view the entire post in your email app.

Thanks for visiting.

Fear Not

When I was a freshman, my high school showed Alfred Hitchcock’s classic horror film, Psycho, in the school auditorium on a snowy Friday night. I desperately wanted to be and look cool, but when Martin Balsam’s Detective Arbogast climbed the stairs in the old house behind Bates Motel to meet Mother, I dove under my seat in terror. Warning: Sixty-four years on, it is still horrifying.

We all face fear. We. All. Face. Fear. “Forty-five on the back of the jersey upon your soul.”

“Fear sells. Fear makes money. The countless companies and consultants in the business of protecting the fearful from whatever they may fear know it only too well. The more fear, the better the sales.”

That short summary, from The Science of Fear, by Dan Gardner, is perfect. Gardner goes on to recount how post-9.11 fear dramatically reduced air travel and led to many, many more driving trips. However, if a 9.11 impact attack had happened every single day for a year, the odds that you’d be killed by such an attack would be one in 7,750, still greater than the actual odds of dying in a traffic accident, which are one in 6,498. Gerd Gigerenzer estimates that the increase in automobile travel in the year after 9.11 resulted in 1,595 more traffic fatalities than would have otherwise occurred.

If you want to make a sale, find a bogey-man, explain why your marks should be terrified of him, tell them who is to blame for the bogy-man’s offenses, and offer a purported remedy.

I shouldn’t have to add that the alleged remedy usually costs. A lot.

Investors face fear every day, although more so on some days than others (nobody complains about volatility to the upside), and don’t often face it very effectively. Markets are driven by narratives more than they are driven by data, which makes us especially susceptible fear-mongering. To quote Jason Zweig paraphrasing Mike Tyson, “investors always have a plan until the market punches them in the face.”

Real fear comes with names, faces, and a story. And oh how we want deliverance from our fears. As Morgan Housel has cautioned: “The business model of the majority of financial services companies relies on exploiting the fears, emotions, and lack of intelligence of customers. The worst part is that the majority of customers will never realize this.”

Which brings me to John Hussman.

Hussman is a smart guy. He is a Stanford Ph.D. who became a professor at the University of Michigan before setting up his own asset management firm. His anticipatory call on the 2008-09 financial crisis was spot-on, brought in lots of money, and made him a ton of money. High on that success, as of September 2010, Hussman managed $6.7 billion.

Unfortunately, the apocalypse was always nigh to him, irrespective of facts and markets. He’s been wrong essentially ever since.

Robert Frost reminded us that “nothing gold can stay” while Hussman keeps insisting that the markets offer fool’s gold (representative Hussman commentary below; analytical example here).

2010: “Investors dangerously underestimate the risk of an abrupt and possibly severe equity market plunge.” That year, Hussman’s flagship fund, Hussman Strategic Growth (HSGFX), lost 3.62 percent while the S&P 500 made 14.82 percent.

2011: “[T]he expected return/risk profile of the stock market has shifted to hard-negative.” That year, as the S&P 500 barely broke even (2.10 percent), HSGFX did worse (1.64 percent).

2012: “The present menu of investment opportunities continues to be among the worst in history.” The S&P earned 15.89 percent that year while HSGFX lost 12.62 percent, among the worst on the Street.

2013: “[S]tock returns prospectively are very low.” HSGFX’s returns were very low that year (-6.62 percent); the S&P’s were very high (32.15 percent).

2014: “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.” The S&P advanced 13.52 percent in 2014; HSGFX declined 8.50 percent.

2015: “Exit now.” The S&P only returned 1.38 percent that year, but HSGFX lost 8.40 percent.

2016: “[C]urrent extremes imply 40-55 percent market losses…. These are not worst-case scenarios, but run-of-the-mill expectations.” The S&P provided 11.77 percent in gains while HSGFX provided 11.49 percent in losses.

2017: “[T]he most broadly overvalued moment in market history.” The S&P moved 21.61 percent higher. HSGFX lost 12.72 percent

2018: “The music is fading out, and a trap-door has opened up in the floor, but they’re still dancing.” It wasn’t a trap-door, but the S&P 500 lost 4.23 percent in 2018 while HSGFX was up 8.78 percent

2019: “[A] projected 50-65 percent market loss over the completion of this cycle is actually somewhat optimistic.” The S&P rebounded to the tune of 31.31 percent. HSGFX went back to losing and was off 18.86 percent – an astonishing differential of 50 points.

2020: “[E]xtreme valuations ... accompanied by extreme overextension.” HSGFX had a good year, up 14.53 percent. The S&P had a better one, up 18.02 percent.

2021: “Nothing so animates a speculative herd as a parabolic price advance in an asset detached from any standard of value. I am convinced that future generations will use the present moment to define the concept of a reckless speculative extreme, in the same way our generation uses ‘1929’ and ‘2000.’” The S&P 500 returned 28.47 percent in 2021. HSGFX declined 0.23 percent.

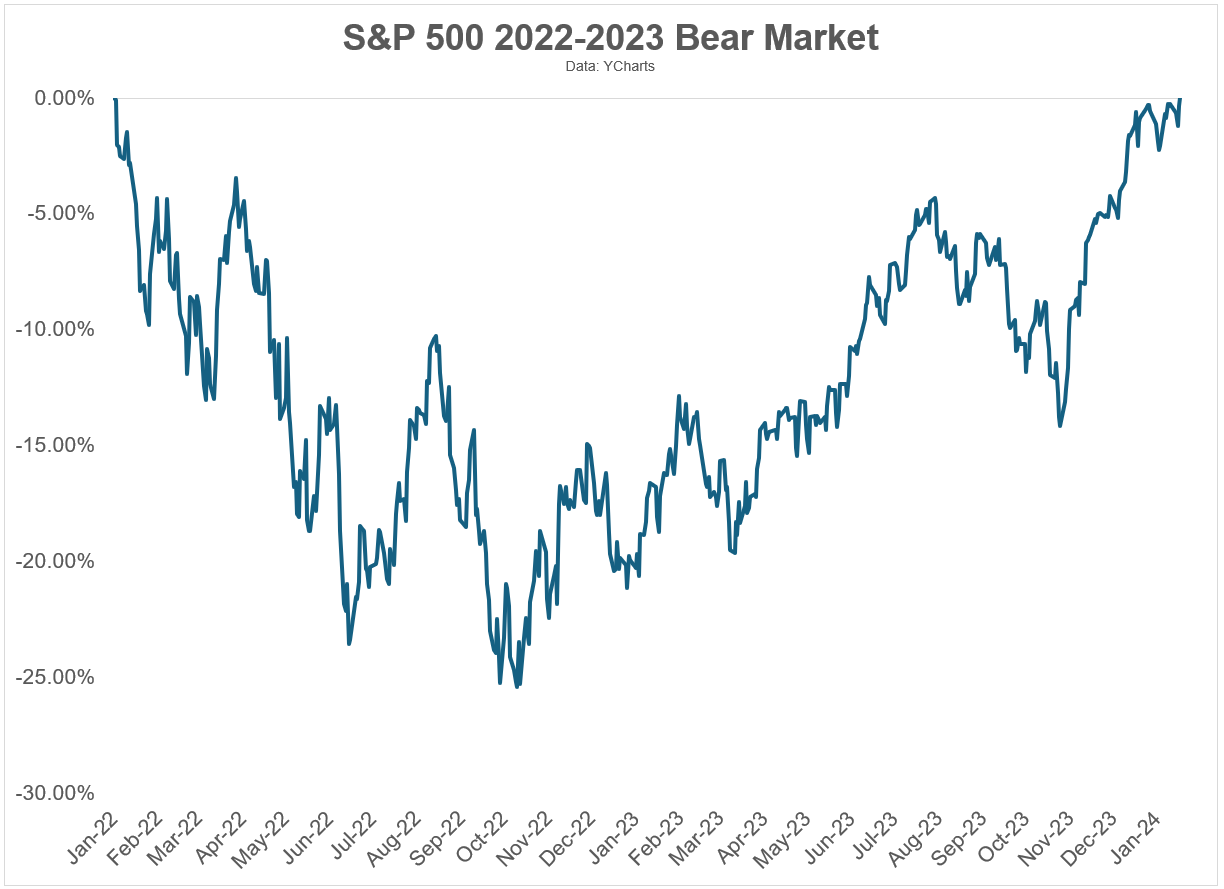

2022: “The recent market decline has simply retraced the frothiest portion of the recent bubble, bringing the most reliable market valuation measures back toward their 1929 and 2000 extremes.” It wasn’t extreme, but the S&P lost 18.04 percent in 2022 and HSGFX did much better, advancing 17.32 percent.

2023: “The last time we observed this combination to a similar degree was in November 2021, shortly before the S&P 500 lost a quarter of its value. ...I remain convinced that this initial market loss will prove to be a small opening act in the collapse of the most extreme yield-seeking speculative bubble in U.S. history.” The S&P 500 was up 26.06 percent in 2023; HSGFX was down 11.61 percent.

2024: “we expect another long, interesting 10-20 year trip to nowhere for the S&P 500.”

Obviously, Hussman turned into a “permabear,” calling for disaster constantly (and wrongly). Hussman still insists that he will be vindicated and criticizes those who would “declare victory at halftime.” He criticized “declaring victory at halftime” six full years earlier, too (so that’s one long halftime).

Hussman wants us to believe that he’s not wrong, merely right but early (if extremely early). However, if you keep making the same wrong call over and over, you don’t get any credit for it when it eventually turns up. After much more than a decade, a “right but early” has to have become “wrong.” Even a stopped clock is right twice per day.

Through 2023, HSGFX has suffered a 10-year average annual “return” of -3.95 percent, annualized, as compared to a 12.03 percent average annual gain by its benchmark, the S&P 500. Despite exceptional early returns, the fund is barely above water since its 2000 inception (+0.55 percent). Notwithstanding this terrible performance, Hussman keeps charging investors more than one percent annually to lose manage their money.

If, a decade ago, you had invested $10,000 in Hussman’s signature fund, you would have lost more than a third of your investment. Meanwhile, the S&P 500 more than tripled in value during that time.

After some surprising clawbacks in Bankruptcy Court, it even appears that those who “invested” in Bernie Madoff’s multi-billion dollar Ponzi scheme, despite major losses due to Madoff’s perfidy, still outperformed those who invested in Hussman’s fund at the same time – by about 10-15 percent.

Not surprisingly, outflows began in earnest in 2011. Hussman’s current assets under management have declined by about 95 percent from $6.7 billion after the financial crisis to $370 million today.

Remember what Barton Biggs, Morgan Stanley’s former strategist, said: “Bullish and wrong and clients are angry; bearish and wrong and they fire you.” Hussman exemplifies the wisdom of legendary investor Peter Lynch, “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

For Hussman, his negativism seems to have evolved over time into an ideological commitment to his rightness, despite the obvious disconfirming evidence, with horrific results.

Still, tomorrow is another day.

“There’s always the hope that this time it’s different,” Hussman says. Hope always seems to spring eternal for underperforming money managers, so long as they are still collecting management fees (a few notable exceptions notwithstanding). Hussman insists he has learned from his mistakes, that he now recognizes that there is no “limit to the recklessness of Wall Street.” But, he mostly blames the Fed (“By relentlessly depriving investors of risk-free return, the Fed has spawned an all-asset financial bubble that now offers return-free risk. Whatever y’all think you’re doing here, it’s not ‘investment’”). Meanwhile, he keeps losing managing other peoples’ money and getting paid handsomely for it, longing for the day when he will – finally – be vindicated.

Hussman is far from the only permabear, of course. Plenty of people try to trade on our fears.

Former Reagan White House Budget Director David Stockman has predicted market crashes in 2012, 2013, 2014, 2015,2016, 2017, 2018, 2019, 2020, 2021, 2022, and 2023. “Dr. Doom,” Marc Faber, he of The Gloom, Boom & Doom Report, regularly and routinely called for corrections and crashes (“bubbles everywhere”) on various media outlets before being exposed as a racist and largely disappearing from view. Others include Jeremy Grantham, Michael Burry, Gary Shilling, Greg Jensen, Nouriel Roubini (the other “Dr. Doom”), Peter Schiff, Stephen Roach, and David Tice.

When they are – eventually, maybe even later today – right, I predict none of them will remind us of the dozens and dozens of times they were wrong.

Permabears exist despite the upward trend of the markets because these alleged oracles garner clicks, eyeballs, attention, television appearances, and assets. It pays.

We respond emotionally to stories. Moreover, fear is the most motivating of emotions, at least in the short-term. As Jeremy Siegel has explained, “Fear has a greater grasp on human action than does the impressive weight of historical evidence.” Warren Buffett has made enormous amounts of money by following the evidence and buying stocks, which have provided consistently high returns on a consistently inconsistent basis for decades: “In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.” Buffett buys stocks and holds them. His “favorite holding period is forever.” The typical investor … not so much.

Even the atypical investor struggles in this regard. As Morgan Housel says, “Every past decline looks like an opportunity, every future decline looks like a risk.” Harry Markowitz won the Nobel Prize for exploring the mathematical tradeoff between risk and return. Some years ago, my friend, Jason Zweig, asked him how, given his work, he structured his own portfolio. He replied: “I visualized my grief if the stock market went way up and I wasn’t in it – or if it went way down and I was completely in it. My intention was to minimize my future regret. So I split my contributions 50/50 between bonds and equities.” That may have been a perfectly appropriate asset allocation for Professor Markowitz, of course, but his thinking was far more fear-based than analytically driven.

As Duke Hall of Fame basketball coach Mike Krzyzewski adds, “Winners hate losing more than [they love] winning.” Per Daniel Kahneman, “the main contribution that Amos Tversky and I made during the study of decision making is a sort of trivial concept, which is that losses loom larger than gains. …As a very rough guideline, if you think two to one, you will be fairly close to the mark in many contexts.”

We are slaves to our past experiences: “Current beliefs depend on the realizations experienced in the past” such that we fear what hurt us before and thus fight the last war (so to speak). Per Kahneman again, “Loss aversion is emotional, the reluctance is emotional, and if I’m making a decision on behalf of somebody else, I don’t feel that emotion, which means, by the way, that advisors are likely to be more rational in the long run because loss aversion is costly.”

FOMO is real too. Accordingly, performance-chasing is widespread, among both retail and institutional investors. Therefore, investor returns significantly trail investment returns.

As Andre Agassi explained, “A win doesn’t feel as good as a loss feels bad, and the good feeling doesn’t last as long as the bad. Not even close.” Or David Letterman: “Maybe life is the hard way, I don’t know. When the show was great, it was never as enjoyable as the misery of the show being bad. Is that human nature?”

Yes, why yes, it is.

When the markets are roiling, and even when they are not, fear is pitched all day, every day, and human nature buys it. It pays a premium, too. A very big premium.

Giving in to the fear we feel is dangerous business, of course, because the market trends solidly upward.

On the other hand, you can always find reasons to be terrified and cash out of the market if you choose to look.

Doing so comes with a crazy-high degree of difficulty. Obviously, market-timing successfully means making multiple immensely difficult and complex decisions and being consistently right. Does that seem like a reasonable expectation to you?

If you don’t want to invest in equities because you fear a market crash, then you shouldn’t be in equities. However, you must also recognize that, if you avoid stocks, you will almost certainly have a lot less money and, the longer you live, the difference between what you have and what you could have had will compound ... a lot.

All of which raises what is likely the crucial question: Are you a long-term investor?

Truly being a long-term investor is difficult because the long-term feels like an eternity in the moment. As Kahneman has explained, “the long-term is not where life is lived.”

Wall Street’s business model is designed to get you to put your money in motion even though time is the one true advantage investors have in the market.

To be clear, none of this is cast in stone. Just because something has always worked doesn’t mean it always will. The worst that has ever happened isn’t a limit on what can happen. Things can always get worse. Past performance is not indicative of future results. If you doubt me, ask Japanese investors how “stocks for the long run” has performed for them, or ask risk managers how VaR worked for them during the GFC.

It should also be noted that the permabears could (finally) be right today. A market crash might be imminent.

But that’s not the way any of us who are long-term investors should bet. The probabilities favor investment, especially for long-term investors. By a lot. Our brains all echo with fearful thoughts, whispers, and imprecations. For most of us, most of the time, we’d do well to ignore them about our investment choices. Instead, we should listen to the Christmas angel, even though Christmas is over, and “fear not.”

No matter how many alleged experts call for the market to crash.

Totally Worth It

Impressive marketing (and, obviously, a nod to the following great song. More examples here.

{kind=link}

Gold bars continue to sell out in hours at Costco, yet, historically, buyers prepping for an apocalypse would have been much better off buying the stock. Costco stock has gained over 116,000 percent since its IPO in December 1985 versus a 413 percent gain for Gold and 228 percent increase in U.S. inflation.

Feel free to contact me via rpseawright [at] gmail [dot] com or on Twitter (@rpseawright) and let me know what you like, what you don’t like, what you’d like to see changed, and what you’d add. Praise, condemnation, and feedback are always welcome.

Of course, the easiest way to share TBL is simply to forward it to a few dozen of your closest friends.

On Friday, January 5, 2024, the day a door plug flew off an Alaska Airlines plane mid-flight and freaked everybody out – 120 Americans died in motor vehicle crashes. Roughly 136 died from opioids. Perhaps 150 died as hospital inpatients due to preventable medical errors. About 230 died of COVID-19, and zero died in aircraft accidents.

You may hit some paywalls below; most can be overcome here.

This is the best thing I read in the last week. The smartest. The saddest. The coolest (unless it’s this). The loveliest.The most important. The most disconcerting. Kentucky. Furries. AI. Please, no. Grandpa. Done with the ‘Boys. Good idea. Obvious errors. Atomic. Bad bets. The best game of chess, ever, was played 25 years ago this week. The politics of lying. RIP, Peter Schikele, the king of joyful absurdity.

Please send me your nominations for this space to rpseawright [at] gmail [dot] com or via Twitter (@rpseawright).

The TBL Spotify playlist, made up of the songs featured here, now includes over 270 songs and about 19 hours of great music. I urge you to listen in, sing along, and turn up the volume.

My ongoing thread/music and meaning project: #SongsThatMove

“Freedom’s just another word for nothin’ left to lose.” A Kris Kristofferson song first recorded by Roger Miller (and a fair number of other artists) before its defining performance by Janice Joplin (released posthumously).

Benediction

“Is it you?”

We live on “a hurtling planet,” the poet Rod Jellema informed us, “swung from a thread of light and saved by nothing but grace.”

To those of us prone to wander, to those who are broken, to those who flee and fight in fear – which is every last lost one of us – there is a faith that offers grace and hope. And may love have the last word. Now and forever. Amen.

As always, thanks for reading.

Issue 164 (January 26, 2024)

Great as ever, Bob. Thanks.

Good post Bob. Thanks for the reminder.